America – home of the free and land of the unhealthy.

Life expectancy in the United States has dropped for the second year in a row, and as of 2012, about half of all American adults had one or more chronic health conditions and 24% had two or more conditions. [1]

Gently put, health and healthcare are both ‘areas of improvement’ for the United States.

Cutting Costs with High Deductible Health Plans

Employers and employees alike have turned to high deductible healthcare plans (HDHPs) as a way of reducing overall healthcare costs.

Coupled with lower monthly premium costs in exchange for higher out-of-pocket deductibles, these plans place more responsibility on the consumer (i.e. the employee) to be thoughtful about their health care spending.

HPHPs can be a great option for young and healthy consumers; however, they may turn into a financially dangerous choice for unsavvy consumers.

Considering that the average deductible for single-coverage with an HDHP is $2,304, it’s easy to see how HDHPs can cause significant financial hardship to your most vulnerable people. [2]

To ensure that employees fully understand the plan coverage, HDHPs should be paired with financial and educational resources for employees.

In this article, we’ll cover five ways that you can support employees’ decision-making process when offering HDHPs.

1. COST-COMPARE HEALTHCARE PLANS

The cost of healthcare continues to rise, straining the wallets of many families.

In fact, 43% of insured adults report difficulties affording their deductible. In 2017, employees with family health plans contributed an average $5,714 of towards their annual premium. This figure has risen 32% since 2012, while wages have only increased 12% during that same period. [3,4]

Employees are tempted to choose the cheapest health plan available, but that approach can backfire.

Not having the right health coverage can leave employees feeling like they’re battling a stormy commute with a kid’s umbrella.

When it comes to bad weather and medical bills, no one wants to get stuck in a torrential downpour.

A recent report found that 77% of consumers admitted to regretting a health decision. The top reason? Not checking and/or comparing costs. [5]

One study of claims data found that the average cost for outpatient surgery at an ambulatory surgery center was 24 times more expensive at an out-of-network facility as compared to an in-network facility. [6]

Mistakes like that can leave the bill feeling worse than the diagnosis.

To help employees avoid any healthcare ‘sticker shock’, provide tools to easily compare the coverage of each plan and the out-of-pocket costs to continuing existing treatment regimens, like prescriptions and specialist visits.

2. SET THE SAVINGS STANDARD & OPTIONS

It’s scary to know that 46% of Americans can’t afford a medical emergency of $400 or more, but discussing medical emergencies with employees doesn’t have to mean gloom and doom.

Unexpected medical bills are a reality of life. They aren’t a matter of ‘if’, but a matter of ‘when’. Your employee’s kid could easily run up a $700 ER bill insisting that a small boo-boo is a broken arm.

Average fourth-quarter 2017 out-of-pocket costs were $1,813 – up 11% from the year prior. On average, 39% of patient out-of-pocket costs per healthcare visit were between $501-$1,000; and 12% were more than $1,000. [8]

Promoting a savings mentality and setting expectations for employees during the open enrollment period can help prevent employee medical emergencies from becoming financial disasters.

The best way to maximize savings for HDHP out-of-pocket medical expenses is with a health savings account (HSA), where both the contributions and earnings are tax-free. HSA funds can be used for future medical expenses, including those accrued in retirement.

Financial Stress & Medical Bills

The relationship between financial stress and health problems is well-documented. Of the 85% of Americans feeling financial anxiety, 67% say it’s negatively impacting their health. [9]

A recent study found that those with significant financial stress are 13 times more likely to suffer from a heart attack. [10]

According to the Center for Financial Services Innovation, “Persistent financial struggles constrain an individual’s resources and can impede cognitive function, both of which impair decisions, and can perpetuate unfavorable financial and physical health situations.” [11]

This evidence is further supported by a 2017 Alight Solutions report which found that those with high stress are more likely to say that healthy living requires too much investment. The number one source of stress? One’s financial situation. [5]

Clearly the stress can perpetuate a cycle of poor health and financial struggle.

3. PROMOTE WAYS TO SAVE FOR HDHP EXPENSES

You work hard to provide employees with the best benefits package that you can, so don’t be shy about promoting it!

Ask your marketing team if they can help spruce up your internal emails.

Be proud to tell your employees about the oh-so-fabulous benefits they can access – however big or small!

In a recent PwC study, fifty-six percent (56%) of millennials reported that their loyalty to their company is influenced by how much the company cares about their financial well-being, and 67% of millennials said they would be attracted to another company that care more about their financial wellbeing. [12]

After all, a penny saved is a penny your employees aren’t complaining about.

4. CONTINUE HDHP EDUCATION FOR EMPLOYEES

For most people, discussing healthcare is like discussing a colleague’s commute. Every minute feels like a lifetime.

Don’t let that discourage you. Expect that employees will, at some point, zone out during those lunch-and- learn presentations. It’s not you, it’s the healthcare talk.

Consider providing more snackable-sized tidbits throughout the year.

In the first or second quarter, provide guidance around researching in- network care options and avoiding unnecessary fees. After tax season, remind employees to address existing health ailments and to set aside money for emergency savings.

One study found that only 40% of healthcare consumers know where to go to figure out what a health service they need or want will cost. Clearly there are knowledge gaps! [5]

Prescription Savings

Healthcare insurers have recently faced major backlash withholding prescription drug rebates and blocking consumer access to cheaper versions of costly prescriptions.

Between bad press and federal investigations, insurers like UnitedHealthcare, have announced that they will pass along drug rebates to consumers, which can help people with high deductibles save anywhere from a few dollars to a few thousand! [13,14]

For that reason, it’s important for consumers to be aware of the drug rebates and cheaper alternatives available for any prescription regiments. Online resources are available to help consumers find manufacturer discounts and the cheapest pharmacy carrying the drug.

Medical Procedures

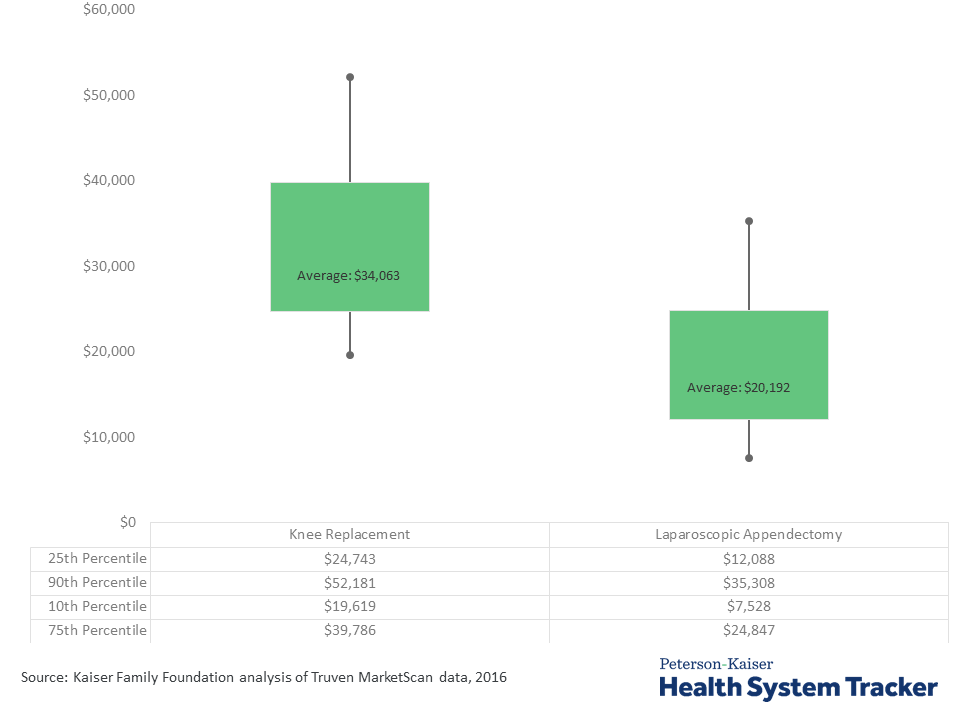

There are large variations in the prices of common medical procedures, such as a knee replacement or laparoscopic appendectomy, as highlighted with the graph below. [15]

Cost Variance of Medical Procedures

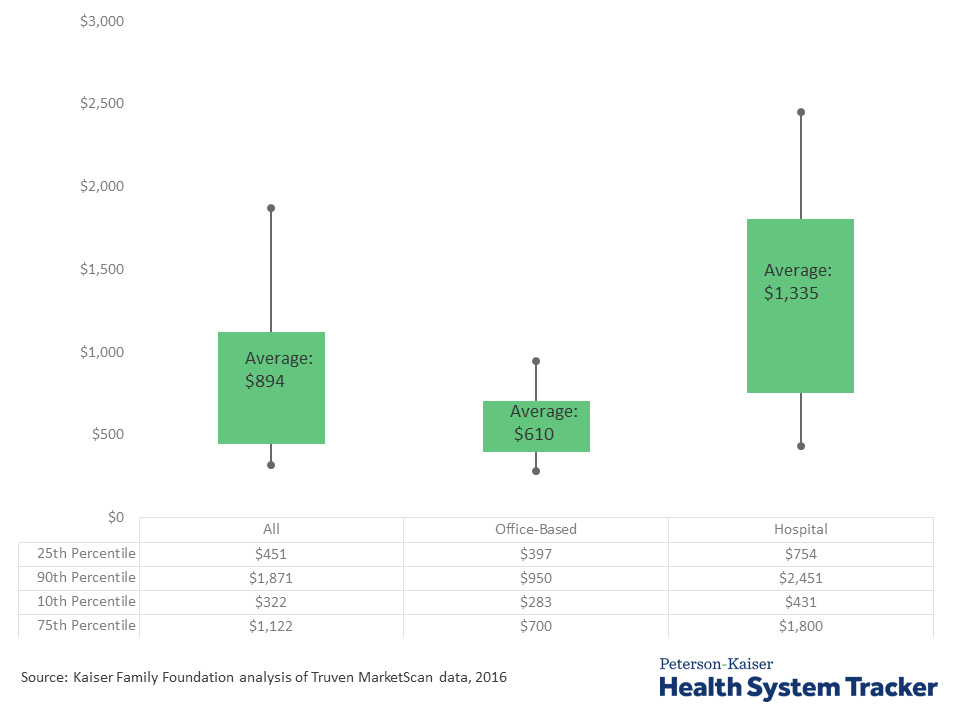

The cost of common medical procedures can also vary based on the location. The graph below shows how magnetic resonance imaging (MRI) prices are higher and variation is greater in hospital settings than in other clinical locations.

Cost Variance of Medical Procedures Based on Location

Most major healthcare providers have cost-calculator tools to help consumers estimate costs for medical procedures. Online websites, such as fairhealthconsumer.org, also provide useful tools for determining expected and fair prices for medical care.

Covering Unexpected Medical Expenses

Given that 78% of Americans live paycheck-to-paycheck and 46% of Americans couldn’t cover an unexpected expense of $400, financially insecure consumers are particularly vulnerable to the potentially high costs associated with HDHPs. [7]

Healthcare costs and other expenses cause many to fall behind financially, and 29% of adults have trouble paying their medical bills. [3]

So where do Americans turn for emergency funds if a medical event does occur?

Up to 27 million U.S. adults are putting medical expenses on credit cards, costing them an average of $471 in interest for a year’s worth of out-of-pocket medical spending. Others are borrowing against their retirement funds, foregoing necessary household purchases, or delaying savings. [16]

In some cases, financial stress or an inability to afford medical expenses cause many to delay or skip care altogether.

A 2017 Kaiser Family Foundation poll found that 27% of respondents said they had postponed medical care in the past year due to costs. This finding is supported by another study, which found that U.S. consumers increased their out-of-pocket health spending by 60% in the week following their tax refund. [17,18]

Delaying medical care is far from a solution, as doing so can quickly turn a small issue into a major problem – and a costlier one at that. Even without delaying care, financial stress by itself can cause health problems.

5. PROVIDE ACCESS TO SOCIALLY RESPONSIBLE CREDIT

Getting employees to financially plan ahead is easier said than done. After all, nothing is a priority until it’s an emergency.

Lack of financial security is a growing concern among Americans, and many delay patient care because they can’t afford the out-of-pocket costs of their HDHPs.

When emergencies strike, employees need access to low-cost credit in order to cover the costs.

To the nay-sayers of this belief, it’s time to dismount the moral high-horse and accept that sometimes borrowing is the best option. When it is, employees need access to socially responsible credit.

At Kashable, we offer employees a financial safety net for life’s unexpected expenses. By working with employers, we can offer low-cost credit to employees across the credit spectrum, protecting your people from high-cost alternatives.

Bringing It All Together

So there it is. Five easy ways to help your employees navigate their HDHPs. Now you can get back to the sixteen other HR tasks sitting on your desk.

When you empower employees with the right financial resources, you better your business.

As a socially-responsible lender, we’re passionate about our mission to help your employees build financial security and to take control of their future.

Tackling Unexpected Medical Bills with Kashable

Kashable is a financial wellness benefit that provides employees with a better way to tackle unexpected medical expenses and costly debt.

By working with employers, Kashable can offer low-cost loans to employees across the credit spectrum, giving them an intelligent alternative to 401(k) loans, credit cards and pay advances. Kashable only lends what employees can afford to borrow, with loans that are repaid automatically through payroll. Welcome to Socially Responsible Credit™.

REFERENCES

- Kochanek, K.D., Murphy, S.L., Jiaquan Xu, M.D., and Elizabeth Arias, Ph.D.”Mortality in the United States, 2016”. National Center for Health Statistics.

- Kaiser Family Foundation. “2017 Health Benefits Survey.”

- Kaiser Family Foundation. “The Burden of Medical Debt: Results from the Kaiser Family Foundation/New York Times Medical Bills Survey”, January 2016.

- Kaiser 2017 Health Benefits Survey

- Alight Solutions. “2017 Consumer Health Mindset Study”.

- StarMark. “Big Cost Savings with In-Network vs. Out-of-Network Care”, 2016.

- Board of Governors of the Federal Reserve System. “Report on the Economic Well-Being of U.S. Households in 2015”, May 2016.

- Wiik, J. “Healthcare Revolution: The Patient is the New Payer”, 2017.

- Northwestern Mutual. “Planning & Progress Study 2016”.

- European Society of Cardiology.”Significant financial stress associated with 13-fold higher odds of having a heart attack”, November 2017.

- Center for Financial Services Innovation. “Employee Financial Health: How Companies Can Invest in Workplace Wellness”, May 2017.

- PricewaterhouseCoopers.”2018 Employee Financial Wellness Survey”.

- Edney, A. (2018, March 7). ‘Rigged’ System Blocks Use of Lower-Cost Drugs, FDA Chief Says. Bloomberg.

- Ableson, R. (2018, March 7). UnitedHealthcare says it will pass on rebates from drug companies to consumers. CNBC.

- Kaiser Family Foundation. “How have healthcare prices grown in the U.S. over time?”, May 2018.

- NerdWallet. “2017 Household Debt Study.”

- Kaiser Family Foundation.“Data Note: Americans’ Challenges with Health Care Costs”, March 2017.

- JP Morgan Chase & Company. “Deferred Care: How Tax Refunds Enable Healthcare Spending”. January 2018.